IMF: To solve inequality, tax food, books and funerals

The IMF has attracted plenty of favourable attention from unfamiliar places with two ‘staff papers’ (we’re enjoined to consider them as the personal opinions of the authors, not the IMF itself, an injunction that we all merrily ignore). The first argues that inequality reduces growth, while redistribution is an effective tool for reducing it; the second explains how governments should use taxes and public expenditure to achieve this goal.

Inequality campaigners are over-the-moon to have the IMF on their side. Oxfam International hails the IMF for “mashing myths and debunking dogma in economic policy,” while the Oxfam inequality guru, Nick Galasso, is fulsome in his praise of an “ideological sea change” at the Fund (“if If it sounds like I have a crush on the IMF’s Managing Director, Christian Lagarde…”).

IMF economists offer countries tools to shrink #inequality http://t.co/fIAoL5IpIH #globaldev

— Oxfam International (@Oxfam) March 16, 2014

But what tools does the IMF think we should use to shrink inequality? Oxfam’s tweet leads to a Reuters article covering a speech by IMF deputy managing director, David Lipton. The speech is definitely worth reading in full – it’s a digestible summary of emerging IMF thinking, while the table on page 43 of the IMF report provides an overview of its suite of policy prescriptions.

Key recommendations for developed countries include substituting means-tested benefits for universal ones; raising the retirement age and making the rich work longer than the poor; charging more for university education in order to spend more on schools; and making income tax more progressive, while eliminating tax breaks.

Many of these are good policies, but let’s not pretend they’re all politically palatable. Take the last one as an example. In the United States, President Obama and the Republicans are locked into fruitless combat on eliminating a few of the most egregious pro-rich tax breaks. A recent revenue-neutral tax reform plan from a Republican has provoked a blizzard of protest from Wall Street and has been roundly condemned by his colleagues.

But the IMF is not interested in these small-bore controversies, it has the big one in its sights: the 37 million Americans who benefit to the tune of $70bn or so from tax relief on their mortgages. And that’s a political live wire. I’d speculate that any presidential candidate – Republican or Democrat – who ran for 2016 on a “tax the homeowners” platform would have as much chance of winning the nomination as I do.

This is not just an American problem. Look at the IMF’s core policy prescription for the United Kingdom – one good enough that it makes it into Lipton’s speech as well as into the report. The UK should move to a flat rate of VAT on all goods and services, Lipton argues, and use the money to increase benefits.

That would mean imposing a 20% tax on food (raising £16bn or so), and on rent and house construction (another £13bn), while increasing tax on household electricity and gas from 5% to 20% (£5bn). Tax would also go up on books, children’s clothing, tampons, condoms, stamps, charities like Oxfam, and… funerals. Yep – the IMF is proposing a burial tax.

All in all, this would give George Osborne £60bn to play with (table 4), more if he axes universal benefits in favour of greater means-testing (goodbye child benefit, winter fuel allowance etc). This would be enough to double benefits for working-age low earners and the unemployed (table 8.2).

Good news for inequality, maybe, but an act of political insanity. In the UK, we once had a manifesto that was derided as ‘the longest suicide note in history’. Flat rate VAT (for all its merits) would be the shortest. VAT on food? On books? On coffins? Just look at the disaster that befell the British government when it tried to tax Cornish pasties to see how badly this would go wrong.

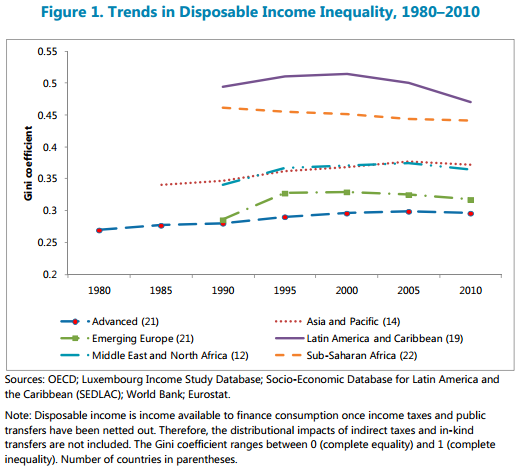

There are equally obvious political bear traps when you look at the problem from the point of view of low and middle income countries. And the task ahead of them is daunting, given that inequality levels are higher in Asia and the Middle East than in the West, and much higher again in Africa and Latin America. A European minister told me that he was hoping for a post-2015 goal that would inspire the whole world to be as equal as his country by 2030. I shudder to think of the collective apoplexy this prospect would cause in the G77.

No-one is pretending that IMF-branded policies represent the final word on inequality. Oxfam issued a media brief this week, which proposes the UK tackles inequality by cracking down on tax dodgers, implementing a Tobin tax and a tax on land, and increasing the minimum wage.

But what the Fund’s excellent report does is underline the importance of going from high-level aspirations to detailed scrutiny of the policies we want governments to implement to bring inequality down. Only then can we understand how today’s high level debate on inequality will play out in the bruising world of retail politics. It would be good to see Oxfam’s proposals costed and their likely impact on inequality audited, so we can see what they’ll deliver and who’d foot the bill. Without that the politics remain hard to read.

A greater focus on policies and implementation, and the politics of both, is especially important for those arguing that we should stop being “belligerent” about the “unrealistic goal” of ending sub-$1.25 a day poverty and instead build a post-2015 agenda on the the more sustainable political foundations that inequality offers.

Sure, we have an ‘emerging consensus’ that something needs to be done to bring inequality down. But will that consensus hold when publics around the world, and assorted lobbyists, get a better sense of what that something looks like?